The question of when the United States began subsidizing fossil fuels is a complex one, as it involves tracing back decades of policies, tax breaks, and direct financial support aimed at promoting the oil, gas, and coal industries. While there is no single definitive year marking the start of these subsidies, many historians and economists point to the early 20th century, particularly the 1918 Revenue Act, which introduced tax provisions benefiting the oil industry, as a significant starting point. Over the years, additional measures such as the depletion allowance, percentage depletion, and various research and development incentives have further entrenched government support for fossil fuels, making it challenging to pinpoint an exact year but clear that subsidies have been a longstanding feature of U.S. energy policy.

| Characteristics | Values |

|---|---|

| Year Subsidies Began | There is no single definitive year the US began subsidizing fossil fuels. Subsidies have evolved over time through various policies and tax provisions. |

| Early Examples | 1916: Depletion allowance introduced, allowing oil and gas companies to deduct a percentage of revenue to account for resource depletion. |

| Significant Expansion | 1926: Percentage depletion allowance increased, providing substantial tax benefits to fossil fuel companies. |

| Post-WWII Era | 1940s-1950s: Further tax breaks and incentives introduced to encourage domestic oil and gas production. |

| Modern Era | Ongoing: Various tax breaks, direct subsidies, and indirect support (e.g., research funding, infrastructure development) continue to benefit the fossil fuel industry. |

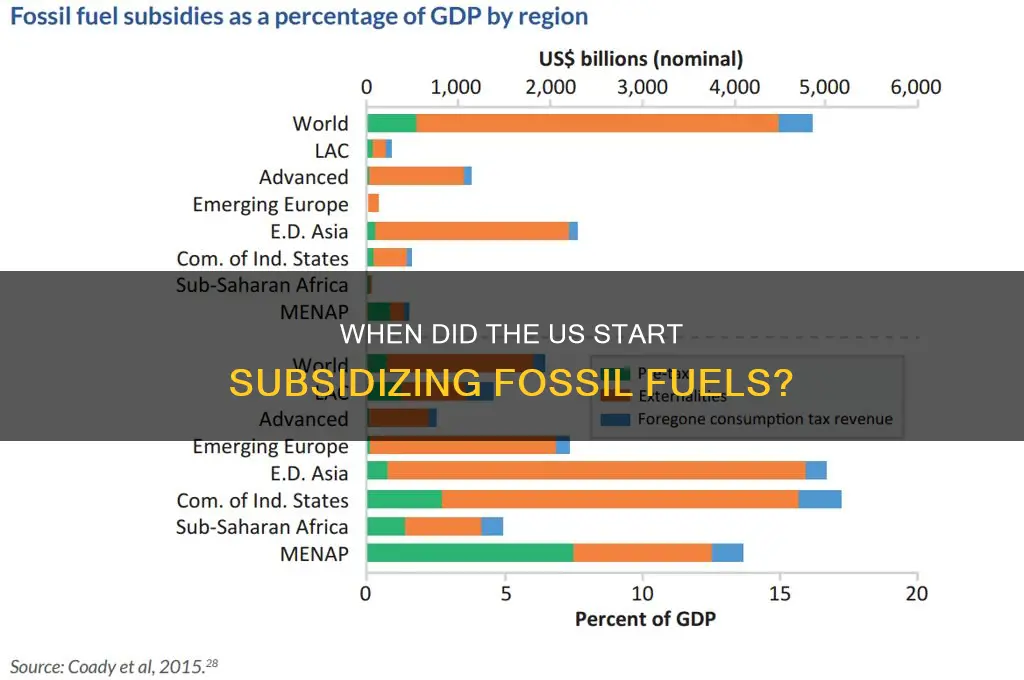

| Estimated Annual Subsidies | $20 billion (varies depending on methodology and definition of subsidies) |

| Forms of Subsidies | Tax breaks, direct payments, loan guarantees, research funding, infrastructure development, price controls |

| Justification | Energy security, economic development, job creation |

| Criticism | Environmental impact, market distortion, hindering renewable energy development |

Explore related products

What You'll Learn

![]()

Origins of Fossil Fuel Subsidies

The origins of fossil fuel subsidies in the United States can be traced back to the early 20th century, when the federal government began implementing policies to support the domestic oil and gas industry. One of the earliest instances of such support was during World War I, when the government recognized the strategic importance of petroleum for military operations. In 1916, the U.S. Bureau of Mines was established to promote the development of domestic mineral resources, including fossil fuels. However, it was not until the 1920s and 1930s that more direct subsidies and tax incentives were introduced to encourage oil and gas exploration and production.

A significant milestone in the history of U.S. fossil fuel subsidies came with the Revenue Act of 1926, which introduced the concept of percentage depletion allowances for oil and gas producers. This tax incentive allowed companies to deduct a percentage of their gross income as a depletion allowance, effectively reducing their taxable income. The percentage depletion allowance was initially set at 27.5% for oil and gas wells, providing a substantial financial benefit to producers. This policy was designed to stimulate domestic production and reduce reliance on imported oil, particularly in the aftermath of World War I.

The 1930s saw further expansion of fossil fuel subsidies, driven by the economic challenges of the Great Depression and the growing recognition of oil's strategic importance. The Connally Hot Oil Act of 1935 and the Petroleum Administrative Board were established to regulate the oil industry and stabilize prices, while also providing indirect support to domestic producers. Additionally, the Public Utility Holding Company Act of 1935 and the Natural Gas Act of 1938 laid the groundwork for federal regulation of the energy sector, creating an environment conducive to further subsidies and incentives.

The post-World War II era marked a significant escalation in U.S. fossil fuel subsidies, as the government sought to secure energy supplies for the growing economy and support the expansion of the automobile industry. The 1940s and 1950s saw the introduction of various tax credits, grants, and low-interest loans for oil and gas exploration and production. Notably, the Mineral Leasing Act of 1920 was amended in 1947 to provide more favorable terms for federal oil and gas leases, further incentivizing domestic production. These policies were reinforced by the strategic considerations of the Cold War, as the U.S. sought to maintain energy independence and support its allies.

By the 1970s and 1980s, fossil fuel subsidies had become deeply entrenched in U.S. energy policy, with a wide range of tax breaks, direct payments, and regulatory advantages benefiting the oil, gas, and coal industries. The Energy Tax Act of 1978 and the Crude Oil Windfall Profits Tax Act of 1980, though initially aimed at generating revenue from the energy sector, ultimately included provisions that continued to support fossil fuel production. These decades also saw the rise of environmental concerns, leading to some debates about the appropriateness of subsidizing fossil fuels, but the overall policy framework remained largely supportive of these industries.

In summary, the United States began subsidizing fossil fuels in a meaningful and sustained manner during the early to mid-20th century, with key policies and legislation introduced in the 1920s, 1930s, and post-World War II era. These subsidies were driven by a combination of economic, strategic, and political factors, and they laid the foundation for the extensive support that the fossil fuel industry continues to receive today. Understanding these origins is crucial for contextualizing current debates about energy policy, climate change, and the transition to renewable energy sources.

Inexhaustible Energy: The Clean, Everlasting Alternative to Fossil Fuels

You may want to see also

Explore related products

![]()

Key Legislation Enabling Subsidies

The United States' history of subsidizing fossil fuels dates back to the early 20th century, with key legislation playing a pivotal role in establishing and expanding these subsidies. One of the earliest and most significant pieces of legislation was the Revenue Act of 1913, which introduced the first federal income tax and included provisions allowing oil and gas companies to deduct certain expenses, effectively reducing their tax burden. While not a direct subsidy, this tax advantage marked one of the first instances of government support for the fossil fuel industry.

A major milestone came with the Mineral Leasing Act of 1920, which allowed private companies to lease public lands for oil and gas extraction at below-market rates. This legislation provided a direct financial benefit to fossil fuel companies by granting them access to valuable resources at reduced costs. The act also established royalty rates that were often lower than those in private contracts, further subsidizing the industry. This marked a clear shift toward government-enabled subsidies for fossil fuel production.

The Depletion Allowance, expanded significantly in the Revenue Act of 1926, became another cornerstone of fossil fuel subsidies. This tax provision allowed oil and gas companies to deduct a percentage of their gross income to account for the depletion of natural resources. The allowance was set at an unusually high rate—27.5% for oil and gas compared to 5% for other industries—providing a substantial financial advantage. This subsidy remained in place for decades, despite periodic debates about its fairness and environmental impact.

During World War II and the post-war era, the Defense Production Act of 1950 further entrenched government support for fossil fuels. While primarily aimed at ensuring resource availability for national defense, the act included provisions that indirectly benefited the oil and gas industry, such as price controls and production incentives. Additionally, the Federal-Aid Highway Act of 1956, which funded the construction of the interstate highway system, spurred increased demand for gasoline, indirectly subsidizing the fossil fuel industry by creating a larger market for its products.

In the late 20th century, the Energy Policy Act of 2005 continued the tradition of subsidizing fossil fuels by providing billions of dollars in tax incentives, loan guarantees, and direct funding for oil, gas, and coal projects. This legislation also included measures to encourage domestic production, such as opening the Arctic National Wildlife Refuge (ANWR) to drilling. While the act also addressed renewable energy, its substantial support for fossil fuels underscored the enduring role of key legislation in enabling these subsidies.

These pieces of legislation collectively illustrate how the U.S. government has consistently provided financial and regulatory support to the fossil fuel industry since the early 1900s. Through tax breaks, access to public lands, and direct incentives, these policies have played a critical role in shaping the nation's energy landscape and contributing to the industry's dominance.

Fossil Fuels: Black or Not?

You may want to see also

Explore related products

![]()

Early Tax Breaks for Oil Companies

The United States' practice of subsidizing fossil fuels, particularly through tax breaks for oil companies, has deep historical roots. One of the earliest and most significant tax breaks for the oil industry dates back to the early 20th century. In 1916, the U.S. government introduced the depletion allowance, a tax deduction that allowed oil companies to deduct a percentage of their gross income to account for the depletion of natural resources. This policy was initially intended to encourage domestic oil production and reduce dependence on foreign oil, but it quickly became a substantial financial benefit for the industry. The depletion allowance effectively reduced the taxable income of oil companies, providing them with a significant competitive advantage and fostering rapid growth in the sector.

The 1920s and 1930s saw further expansion of tax breaks for oil companies, solidifying their role in the U.S. economy. During this period, the percentage depletion allowance was increased, allowing companies to deduct up to 27.5% of their gross income from oil and gas production. This generous deduction was justified as a means to incentivize exploration and production, particularly in the aftermath of World War I, when energy security became a national priority. Additionally, the introduction of the intangible drilling costs (IDC) deduction in the 1910s and its expansion in subsequent decades allowed companies to write off expenses related to drilling and development in the year they were incurred, rather than over the life of the well. These early tax breaks were instrumental in shaping the oil industry's dominance in the U.S. energy landscape.

By the mid-20th century, these tax breaks had become entrenched in U.S. fiscal policy, despite growing criticism from economists and environmentalists. The 1950s and 1960s saw continued support for the oil industry through these mechanisms, even as other sectors faced more stringent tax regulations. The percentage depletion allowance, in particular, remained a cornerstone of oil company finances, enabling them to reinvest profits into further exploration and expansion. This era also saw the oil industry's lobbying efforts intensify, ensuring that these tax breaks were preserved and, in some cases, expanded, despite periodic attempts at reform.

The legacy of these early tax breaks is still evident today, as they laid the foundation for ongoing subsidies to the fossil fuel industry. While some reforms have been implemented over the decades, such as the partial phase-out of the percentage depletion allowance for larger companies in the 1970s, many of these tax benefits remain in place. The IDC deduction, for example, continues to provide oil companies with significant tax advantages, allowing them to deduct a wide range of expenses immediately. These early policies not only shaped the economic trajectory of the oil industry but also contributed to its political influence, making it challenging to enact meaningful changes to fossil fuel subsidies in the United States.

In summary, the U.S. began subsidizing fossil fuels through tax breaks for oil companies as early as the 1910s, with the introduction of the depletion allowance and other deductions. These policies were designed to promote domestic oil production but evolved into long-standing financial benefits for the industry. By the mid-20th century, these tax breaks were firmly established, supported by strong industry lobbying and embedded in the nation's fiscal framework. Their enduring impact highlights the challenges of reforming fossil fuel subsidies, even as the need for a transition to cleaner energy sources becomes increasingly urgent.

Is Oil a Fossil Fuel? Unraveling the Energy Source Debate

You may want to see also

Explore related products

![]()

Post-WWII Energy Policy Shifts

The period following World War II marked a significant turning point in U.S. energy policy, driven by economic growth, geopolitical considerations, and the increasing demand for energy. As the nation transitioned from a wartime economy to a consumer-driven society, the federal government began to implement policies that favored the expansion of fossil fuel industries. While direct subsidies to fossil fuels are difficult to pinpoint to a single year, the post-WWII era saw the introduction of tax incentives, regulatory support, and infrastructure investments that effectively subsidized these industries. One of the earliest and most impactful policies was the 1947 Oil Depletion Allowance, which allowed oil and gas companies to deduct a percentage of their gross income as a tax write-off, ostensibly to account for the depletion of natural resources. This policy provided a financial advantage to fossil fuel producers and encouraged increased domestic production.

The 1950s further solidified the U.S. government's commitment to fossil fuels as the backbone of its energy strategy. The Federal-Aid Highway Act of 1956, signed by President Eisenhower, allocated billions of dollars to build the Interstate Highway System. While not a direct subsidy to fossil fuels, this massive infrastructure project spurred automobile dependency and, by extension, increased demand for gasoline. Simultaneously, the government maintained low gasoline taxes, ensuring that the cost of driving remained affordable for consumers. These policies collectively created an environment where fossil fuels became deeply embedded in the American economy and way of life.

The 1960s and 1970s introduced new challenges, including the Arab Oil Embargo of 1973, which highlighted the nation's vulnerability to foreign oil dependence. In response, the U.S. government doubled down on policies to support domestic fossil fuel production. The Energy Policy and Conservation Act of 1975 and the Powerplant and Industrial Fuel Use Act of 1978 aimed to reduce oil consumption in power plants and encourage the use of coal, a domestically abundant resource. Additionally, the Crude Oil Windfall Profit Tax Act of 1980, though intended to tax oil companies' excess profits, was repealed in 1988, further illustrating the government's reluctance to impose financial burdens on the fossil fuel industry.

Throughout this period, the U.S. government also provided indirect subsidies through research and development funding, such as the Synthetic Fuels Corporation established in 1980, which aimed to develop alternative fuels from coal and oil shale. While this initiative was short-lived, it reflected the ongoing commitment to fossil fuel-based energy solutions. By the late 20th century, the cumulative effect of these policies had firmly established fossil fuels as the dominant energy source in the U.S., with government support playing a critical role in their growth and sustainability.

In summary, while there is no single year that marks the beginning of U.S. subsidies for fossil fuels, the post-WWII era saw a series of policy shifts that effectively subsidized these industries. From tax incentives like the Oil Depletion Allowance to infrastructure projects like the Interstate Highway System, these policies created an environment where fossil fuels thrived. The geopolitical and economic priorities of the time ensured that government support for fossil fuels remained a cornerstone of U.S. energy policy, shaping the nation's energy landscape for decades to come.

How No-Till Farming Saves on Fossil Fuel Costs

You may want to see also

Explore related products

![]()

Impact of the Revenue Act of 1913

The Revenue Act of 1913, a pivotal piece of legislation in U.S. history, laid the groundwork for significant economic and environmental policies, including the indirect subsidization of fossil fuels. While the act itself was primarily focused on establishing the federal income tax and lowering tariffs, its broader economic implications set the stage for future policies that would benefit the fossil fuel industry. The act, signed into law by President Woodrow Wilson, aimed to shift the federal government’s revenue reliance from tariffs to income taxes, thereby modernizing the tax system. This shift had far-reaching effects on industrial sectors, including energy, by creating a more stable fiscal environment that encouraged investment and growth.

One of the indirect impacts of the Revenue Act of 1913 was its contribution to the economic conditions that allowed the fossil fuel industry to thrive. By reducing tariffs, the act made it easier for industries to import and export goods, including machinery and equipment essential for oil and coal extraction. This facilitated the expansion of fossil fuel operations, particularly in regions like Texas and Pennsylvania, where oil and coal were abundant. Additionally, the act’s focus on income tax rather than corporate taxes initially provided a financial cushion for energy companies, enabling them to reinvest profits into exploration and infrastructure development.

The Revenue Act of 1913 also set a precedent for federal intervention in the economy, which would later be used to directly and indirectly support the fossil fuel industry. While the act itself did not include specific subsidies for fossil fuels, it established a framework for government involvement in economic sectors. Subsequent policies, such as the depletion allowance introduced in the 1920s, built upon this foundation by providing tax benefits to oil and gas companies, effectively subsidizing their operations. This allowance allowed companies to deduct a portion of their gross income to account for the depletion of natural resources, reducing their tax burden and increasing profitability.

Another significant impact of the Revenue Act of 1913 was its role in fostering a pro-business environment that prioritized industrial growth over environmental concerns. By stabilizing federal revenue and reducing tariffs, the act encouraged rapid industrialization, including the expansion of fossil fuel extraction and consumption. This focus on economic development laid the groundwork for a century of policies that prioritized energy production over sustainability, delaying the transition to renewable energy sources. The act’s legacy is thus intertwined with the early stages of fossil fuel subsidization, even if indirectly.

In conclusion, while the Revenue Act of 1913 did not explicitly begin the subsidization of fossil fuels, its economic and policy implications were instrumental in creating an environment conducive to the industry’s growth. By modernizing the tax system, reducing tariffs, and fostering industrial expansion, the act indirectly supported the fossil fuel sector. Subsequent policies, such as the depletion allowance, built upon this foundation, solidifying federal support for fossil fuels. Understanding the act’s impact is crucial for tracing the origins of U.S. energy policy and its long-term environmental consequences.

Fossil Fuel Combustion's Devastating Impact on Marine Ecosystems Explained

You may want to see also

Frequently asked questions

The US began providing significant subsidies to the fossil fuel industry in the early 20th century, with notable increases during World War II and the post-war era.

Yes, policies like the Revenue Act of 1913 and the Oil Depletion Allowance of 1926 are often cited as early examples of fossil fuel subsidies in the US.

While not direct funding, the government provided tax breaks, deductions, and incentives that effectively subsidized the fossil fuel industry starting in the 1920s.

World War II led to increased government support for fossil fuels, including price controls and infrastructure investments, to ensure energy security for the war effort.

Yes, the US continues to provide subsidies to the fossil fuel industry through tax breaks, research funding, and other incentives, though the debate over their reduction or elimination persists.

![The History of Sound [Blu-Ray]](https://m.media-amazon.com/images/I/01RmK+J4pJL._AC_UY218_.gif)