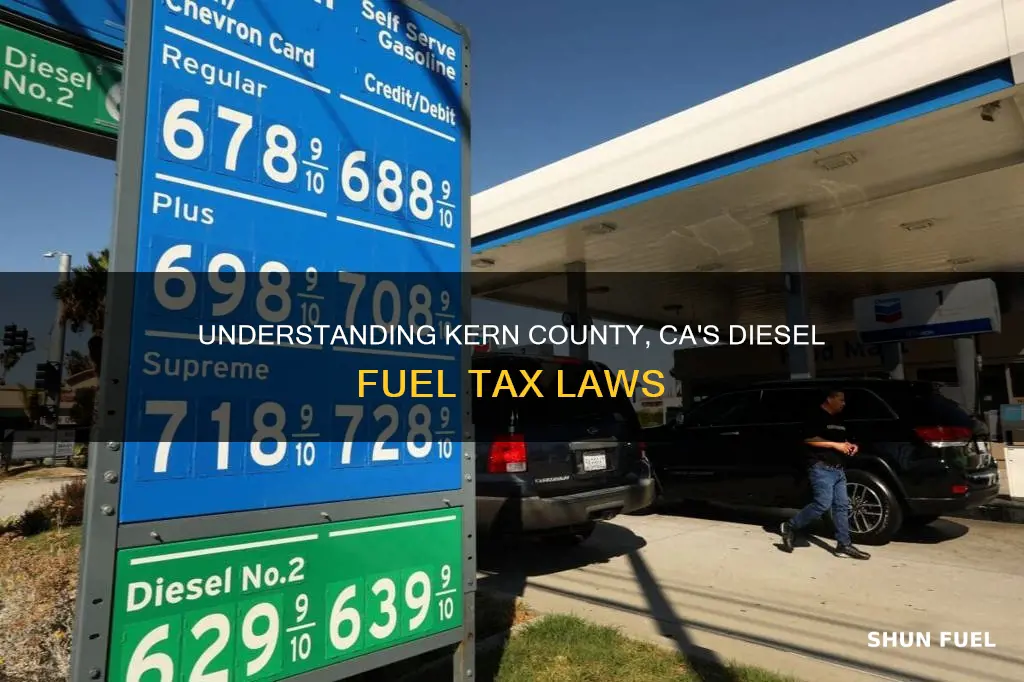

In California, the state collects excise taxes from diesel fuel suppliers before they deliver fuel to retail stations. The Motor Vehicle Fuel Tax Law (MVFTL) and the Diesel Fuel Tax Law impose excise taxes on diesel fuel when it is removed from the refinery or terminal rack, enters the state, or is sold to an unlicensed person. The diesel fuel tax revenue is deposited into the Motor Vehicle Fuel Account in the Transportation Tax Fund, with the balance transferred to the Highway Users Tax Account and local county road funds. Kern County, as a local county, may levy its own charges on diesel fuel, which is calculated as a percentage of the fuel purchase and varies based on the price of fuel.

| Characteristics | Values |

|---|---|

| Type of tax | Excise tax |

| Who pays the tax | Fuel vendors, who pass it on in the fuel's retail price |

| Where does the revenue go | Motor Vehicle Fuel Account in the Transportation Tax Fund, Highway Users Tax Account, State Highway Account, city and county road funds |

| Applicable laws | Motor Vehicle Fuel Tax Law (MVFTL), Diesel Fuel Tax Law, Diesel Fuel Law, Use Fuel Tax Law, Regulation 1598, Motor Vehicle and Aircraft Fuels |

| Tax rate | Not stated explicitly; varies based on the price of fuel |

| Tax exemptions | Dyed Diesel (unless used on a highway), Aviation Gasoline used to propel aircraft |

| Tax refunds | Claims can be filed within three years from the due date of the return on which overpayment was made, within six months from the date of overpayment, within six months from the date a determination became final, or within three years from the date of an involuntary payment |

Explore related products

$64.25 $82.67

What You'll Learn

![]()

Kern County diesel tax revenue funds

In California, the state collects excise taxes from diesel suppliers before they deliver fuel to retail stations. The diesel fuel tax revenue is deposited into the Motor Vehicle Fuel Account in the Transportation Tax Fund. The balance of the revenue is then transferred to the Highway Users Tax Account, which is then transferred to the State Highway Account. Local shares are also transferred to the city and county road funds to construct and maintain public roads and mass transit systems.

The Motor Vehicle Fuel Tax Law (MVFTL) and the Diesel Fuel Tax Law impose excise taxes on diesel fuel when the following events occur: removal at the refinery or terminal rack, entry into the state, sale to an unlicensed person, or the removal or sale of blended motor vehicle fuel or diesel fuel in the state by the blender. The Diesel Fuel backup tax is imposed on the delivery of specific types of diesel fuel into the fuel tank of a diesel-powered highway vehicle.

The price of motor fuel sold in California includes federal motor fuel excise taxes, which are paid to the Internal Revenue Service (IRS) and are used to support the Federal Highway Administration. The federal excise tax rates on various motor fuel products include a 0.1 ¢ per gallon charge for the Leaking Underground Storage Tank Trust Fund (LUST). In most areas, state and federal excise taxes amount to about 13% of the cost of a gallon of gas.

In Kern County, the diesel tax revenue funds are likely used for similar purposes as in the rest of California, including constructing and maintaining public roads and mass transit systems. The funds are also likely transferred to the state and federal governments for use in the Highway Users Tax Account and the Federal Highway Administration, respectively.

Fuel-Efficient Diesel Tractors: Best for Your Farm

You may want to see also

Explore related products

![]()

Diesel tax refund claims

In California, excise taxes are levied on gasoline and diesel fuel in the following circumstances:

- Removal at the refinery or terminal rack

- Entry into the state

- Sale to an unlicensed person

- Removal or sale of blended motor vehicle fuel or diesel fuel in the state by the blender

The state also imposes a backup diesel fuel tax on the delivery of fuel into the tank of a diesel-powered highway vehicle in the following cases:

- When the fuel contains dye

- When a claim for a refund has been allowed

- When a liquid has not been taxed by the Diesel Fuel Tax Law, MVF tax law, or Use Fuel Tax Law

The revenue generated from diesel fuel taxes is deposited into the Motor Vehicle Fuel Account in the Transportation Tax Fund, which is used to pay refunds authorized by the Diesel Fuel Tax Law. The remaining balance is transferred to the Highway Users Tax Account and the State Highway Account, with local shares going towards the construction and maintenance of public roads and mass transit systems.

For diesel tax refund claims, the deadline to file a timely claim is the last of the following dates:

- Three years from the due date of the return on which you overpaid the tax

- Six months from the date of overpayment

- Six months from the date a determination (billing) became final

- Three years from the date of an involuntary payment, such as a levy or lien

It is important to note that if the refund claim is not filed by the applicable deadline, it will not be considered, even in cases of overpayment.

The current and historical tax rates for diesel fuel in California can be found on the Tax Rates—Special Taxes and Fees webpage. Additionally, the CDTFA website provides resources and guides to help businesses navigate the diesel fuel supply chain and understand their tax obligations.

Storing Diesel Fuel: 55-Gallon Drum Storage

You may want to see also

Explore related products

![]()

Diesel tax rates

In California, the state collects excise taxes from diesel suppliers before they deliver fuel to retail stations. The Motor Vehicle Fuel Tax Law (MVFTL) and the Diesel Fuel Tax Law impose excise taxes on diesel fuel when any of the following events occur: removal at the refinery or terminal rack; entry into the state; sale to an unlicensed person; or the removal or sale of blended motor vehicle fuel or diesel fuel in this state by the blender. The diesel fuel tax revenue is deposited into the Motor Vehicle Fuel Account in the Transportation Tax Fund. The balance of the revenue is transferred to the Highway Users Tax Account, which is then transferred to the State Highway Account, and local shares are transferred to the city and county road funds.

The federal government and individual states levy excise taxes to maintain roads and highways. The price of motor fuel sold in California includes federal motor fuel excise taxes, which are paid to the Internal Revenue Service (IRS) and are used to support the Federal Highway Administration. The federal excise tax rates on various motor fuel products are included in the Gasoline, Diesel/Kerosene, and Compressed Natural Gas rates, which include a 0.1 ¢ per gallon charge for the Leaking Underground Storage Tank Trust Fund (LUST). In most areas, state and federal excise taxes amount to about 13% of the cost of a gallon of gas.

Five states charge sales tax on diesel fuel, which is calculated as a percentage of the fuel purchase and varies based on the price of fuel. Biodiesel, waste vegetable oil (WVO), and straight vegetable oil (SVO) are taxed at the same rate as diesel fuel. Dyed Diesel is not subject to Excise Taxes unless used on the highway. When used off-road, Dyed Diesel is taxed at the combined statewide sales tax rate, plus applicable district taxes.

Lucas Fuel Treatment: A Diesel Engine's Best Friend?

You may want to see also

Explore related products

![]()

Diesel tax law

The state of California levies excise taxes on gasoline and diesel suppliers before they deliver fuel to retail stations. These taxes are paid to the Internal Revenue Service (IRS) and are used to support the Federal Highway Administration. The Diesel Fuel Tax Law imposes excise taxes on diesel fuel in the following events: removal at the refinery or terminal rack, entry into the state, sale to an unlicensed person, and the removal or sale of blended diesel fuel in the state by the blender.

The diesel fuel tax revenue is deposited into the Motor Vehicle Fuel Account in the Transportation Tax Fund to pay for refunds authorized by the Diesel Fuel Tax Law. The balance of the revenue is transferred to the Highway Users Tax Account, which is then transferred to the State Highway Account. Local shares are also transferred to the city and county road funds to construct and maintain public roads and mass transit systems.

The Diesel Fuel Tax Law also contains a backup tax, which is imposed on the delivery into the fuel tank of a diesel-powered highway vehicle of any diesel fuel that contains dye, any diesel fuel on which a refund has been allowed, or any liquid on which tax has not been imposed by the Diesel Fuel Tax Law.

The price of motor fuel sold in California includes federal motor fuel excise taxes, which are collected from the manufacturer by the IRS. These taxes are used to support the Federal Highway Administration and include a 0.1 cents per gallon charge for the Leaking Underground Storage Tank Trust Fund (LUST). In most areas, state and federal excise taxes amount to about 13% of the cost of a gallon of gas.

It is important to note that the taxation of diesel fuel in California has evolved over time. For example, dyed diesel, which is not subject to excise taxes unless used on highways, previously fell under the Use Fuel Tax Law but was moved to the Diesel Fuel Tax Law effective July 1, 1995. Additionally, biodiesel, waste vegetable oil (WVO), and straight vegetable oil (SVO) are taxed at the same rate as diesel fuel.

Understanding the Oil-to-Diesel Ratio: A Comprehensive Guide

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

Diesel tax licenses

In California, the state collects excise taxes from diesel suppliers before they deliver fuel to retail stations. The Motor Vehicle Fuel Tax Law (MVFTL) and the Diesel Fuel Tax Law impose excise taxes on diesel fuel when any of the following events occur: removal at the refinery or terminal rack, entry into the state, sale to an unlicensed person, or the removal or sale of blended motor vehicle fuel or diesel fuel in the state by the blender.

The diesel fuel tax revenue is deposited into the Motor Vehicle Fuel Account in the Transportation Tax Fund, with the balance transferred to the Highway Users Tax Account and the State Highway Account. Local shares are also transferred to city and county road funds to construct and maintain public roads and mass transit systems.

The Diesel Fuel & Motor Vehicle Fuel Supplier page provides detailed information on the imposition of tax on the various categories of suppliers. The Diesel Fuel Tax and Motor Vehicle Fuel Tax Laws also contain a backup tax, which is imposed on the delivery of certain types of diesel fuel into the fuel tank of a diesel-powered highway vehicle.

The California Department of Tax and Fee Administration (CDTFA) provides resources for fuel tax and fee guides, including information on current and historical fuel tax and fee rates, as well as a glossary of motor fuel terms. The CDTFA website also offers a "Verify a Permit or License" application to verify a diesel fuel and motor vehicle fuel supplier license.

While the search results did not provide specific information about diesel fuel tax rates in Kern County, California, it is important to note that counties and even individual cities or towns can levy their own charges, which may result in varying tax rates across different regions.

Diesel Fuel Prices in Canada: How High Will They Go?

You may want to see also

Frequently asked questions

The diesel fuel tax rate in Kern County, California, is not available. However, the state excise tax on diesel fuel in California is included in the fuel's retail price.

Vendors pay the diesel fuel tax in California, and this is passed on to consumers in the retail price.

The money from the diesel fuel tax in California goes into the Motor Vehicle Fuel Account in the Transportation Tax Fund. It is used to pay refunds and construct and maintain public roads and mass transit systems.

The diesel fuel tax and the motor vehicle fuel tax are two separate taxes in California. The motor vehicle fuel tax is imposed on the removal of motor vehicle fuel from a terminal rack in California.

To get a refund for overpayment of diesel fuel tax in California, you must file a claim within three years of the due date of the return on which you overpaid the tax, or within six months of the date you overpaid. You can find more information on the CDTFA website.

![(Old Version) H&R Block Tax Software Deluxe + State 2024 with Refund Bonus Offer (Amazon Exclusive) Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51+fonAXhPL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![[OLD VERSION] TurboTax Home & Business 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71b5aAzdXOL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)