Bunker fuel costs refer to the expenses associated with purchasing and using fuel for marine vessels, particularly large ships like cargo carriers and tankers. Bunker fuel, typically heavy fuel oil (HFO) or marine diesel oil (MDO), is essential for powering ship engines and is a significant operational cost in the maritime industry. Fluctuations in global oil prices, environmental regulations, and fuel quality standards directly impact bunker fuel costs, making them a critical factor for shipping companies in managing their budgets and profitability. Understanding these costs is vital for stakeholders, as they influence freight rates, trade routes, and the overall economics of global shipping.

| Characteristics | Values |

|---|---|

| Definition | Bunker fuel costs refer to the expenses incurred by shipping companies for purchasing fuel oil used to power marine vessels. |

| Fuel Types | Primarily includes Heavy Fuel Oil (HFO), Marine Gas Oil (MGO), and Low Sulphur Fuel Oil (LSFO). |

| Current Price (as of October 2023) | HFO: ~$450-$500 per metric ton, MGO: ~$800-$900 per metric ton, LSFO: ~$600-$700 per metric ton. |

| Sulphur Content | HFO: Typically 3.5% or less, LSFO: 0.5% or less (compliant with IMO 2020 regulations). |

| Price Drivers | Crude oil prices, refinery margins, regional demand, environmental regulations, and geopolitical events. |

| Consumption | Large container ships consume ~200-300 metric tons of fuel per day. |

| Cost Impact | Bunker fuel costs account for 50-60% of total voyage expenses for shipping companies. |

| Hedging | Companies often use fuel hedging strategies to mitigate price volatility. |

| Environmental Impact | High sulphur fuels contribute to air pollution, driving the shift to low-sulphur alternatives. |

| Regional Variations | Prices vary by region due to availability, taxes, and local regulations (e.g., Singapore, Rotterdam, Fujairah). |

| Future Trends | Increasing adoption of alternative fuels like LNG, biofuels, and ammonia to reduce carbon emissions. |

Explore related products

What You'll Learn

- Price Fluctuations: Factors driving bunker fuel price changes, including crude oil, demand, and geopolitical events

- Fuel Types: Comparison of costs between HFO, MGO, LNG, and alternative bunker fuels

- Regional Variations: How bunker fuel prices differ across major ports and shipping routes

- Cost Management: Strategies for reducing bunker fuel expenses, such as hedging and slow steaming

- Environmental Impact: How emissions regulations and carbon taxes affect bunker fuel costs

![]()

Price Fluctuations: Factors driving bunker fuel price changes, including crude oil, demand, and geopolitical events

Bunker fuel prices are notoriously volatile, with fluctuations that can significantly impact shipping costs and global trade. Understanding the key drivers behind these price changes is essential for anyone involved in the maritime industry. The primary factor influencing bunker fuel costs is the price of crude oil, which accounts for a substantial portion of the fuel’s production expenses. When crude oil prices rise, bunker fuel costs follow suit, often with a lag of a few weeks as the market adjusts. Conversely, a drop in crude oil prices can lead to temporary relief for shipping companies, though this is rarely sustained without broader economic shifts.

Beyond crude oil, demand dynamics play a critical role in bunker fuel price fluctuations. Seasonal variations, such as increased shipping activity during holiday seasons or reduced demand in economic downturns, directly affect fuel prices. For instance, during the peak shipping season in the fourth quarter, bunker fuel demand spikes, driving prices upward. Additionally, long-term trends like the shift toward greener shipping practices can reduce demand for traditional bunker fuels, though this transition is gradual and varies by region. Monitoring these demand patterns allows stakeholders to anticipate price movements and plan accordingly.

Geopolitical events introduce an unpredictable element to bunker fuel pricing, often causing sudden and dramatic shifts. Conflicts in oil-producing regions, sanctions on major suppliers, or disruptions to key shipping routes can restrict supply, leading to price spikes. For example, the 2022 Russia-Ukraine conflict caused significant volatility in global oil markets, which rippled through bunker fuel prices. Similarly, tensions in the Middle East or blockades in strategic waterways like the Suez Canal can create immediate supply concerns, driving costs upward. Staying informed about geopolitical developments is crucial for mitigating risks associated with these price fluctuations.

To navigate these complexities, shipping companies can adopt strategies such as fuel hedging, which locks in prices for future purchases, reducing exposure to volatility. Diversifying fuel sources and exploring alternative fuels, like liquefied natural gas (LNG) or biofuels, can also provide long-term cost stability. Additionally, leveraging real-time market data and analytics tools enables companies to make informed decisions, optimizing fuel procurement and reducing operational costs. While price fluctuations are inevitable, proactive measures can minimize their impact on the bottom line.

Fuel-Efficient Tires: How Rolling Resistance Saves Gas and Money

You may want to see also

Explore related products

![]()

Fuel Types: Comparison of costs between HFO, MGO, LNG, and alternative bunker fuels

Bunker fuel costs are a critical factor in maritime operations, directly impacting the profitability of shipping companies. Among the various fuel types—Heavy Fuel Oil (HFO), Marine Gas Oil (MGO), Liquefied Natural Gas (LNG), and alternative bunker fuels—each presents distinct cost profiles shaped by market dynamics, regulatory compliance, and technological advancements. Understanding these differences is essential for optimizing fuel strategies in a rapidly evolving industry.

Heavy Fuel Oil (HFO) remains the dominant bunker fuel due to its low cost, typically priced 20-30% below MGO. Derived from the residuals of crude oil refining, HFO’s affordability stems from its high sulfur content and lower demand for processing. However, its use is increasingly restricted under International Maritime Organization (IMO) regulations, which mandate sulfur limits of 0.5% in most regions. Non-compliance incurs penalties, while compliance often requires costly scrubber installations or switching to more expensive low-sulfur alternatives, eroding HFO’s cost advantage.

Marine Gas Oil (MGO), a distillate fuel, is cleaner-burning and compliant with sulfur regulations, but its cost is significantly higher than HFO, often doubling or tripling in price. MGO’s premium reflects its refined nature and lower sulfur content (≤0.1%). For short-haul routes or vessels operating in Emission Control Areas (ECAs), MGO is a practical choice despite its expense. However, for long-haul operations, its cost-per-energy-unit makes it less sustainable, driving interest in alternative solutions.

Liquefied Natural Gas (LNG) emerges as a competitive alternative, offering a 10-20% cost advantage over MGO and near-zero sulfur emissions. LNG’s price volatility, tied to natural gas markets, introduces risk but also opportunity. Its adoption requires substantial upfront investment in infrastructure and vessel modifications, yet long-term savings and regulatory compliance make it an attractive option for newbuilds and retrofits. For instance, a 10,000 TEU container ship converting to LNG can reduce fuel costs by $1-2 million annually, depending on route and market conditions.

Alternative bunker fuels, such as biofuels, methanol, and ammonia, represent the frontier of cost and sustainability. Biofuels, derived from organic matter, offer a drop-in solution with costs comparable to MGO but with lower lifecycle emissions. Methanol, produced from natural gas or renewable sources, is gaining traction due to its simplicity in storage and combustion, though current costs are 10-15% higher than LNG. Ammonia, a carbon-free fuel, holds promise for decarbonization but remains in the pilot phase, with production costs 2-3 times higher than conventional fuels. These alternatives require scalable production and regulatory support to become cost-competitive.

In summary, the choice of bunker fuel hinges on balancing immediate costs, regulatory compliance, and long-term sustainability. HFO remains the cheapest but faces regulatory headwinds, MGO offers compliance at a premium, LNG provides a middle ground with infrastructure challenges, and alternative fuels represent the future with evolving cost dynamics. Strategic decision-making, informed by market trends and vessel-specific needs, is key to navigating this complex landscape.

Science's Dark Legacy: Unraveling Racism's Roots in Historical Research

You may want to see also

Explore related products

![]()

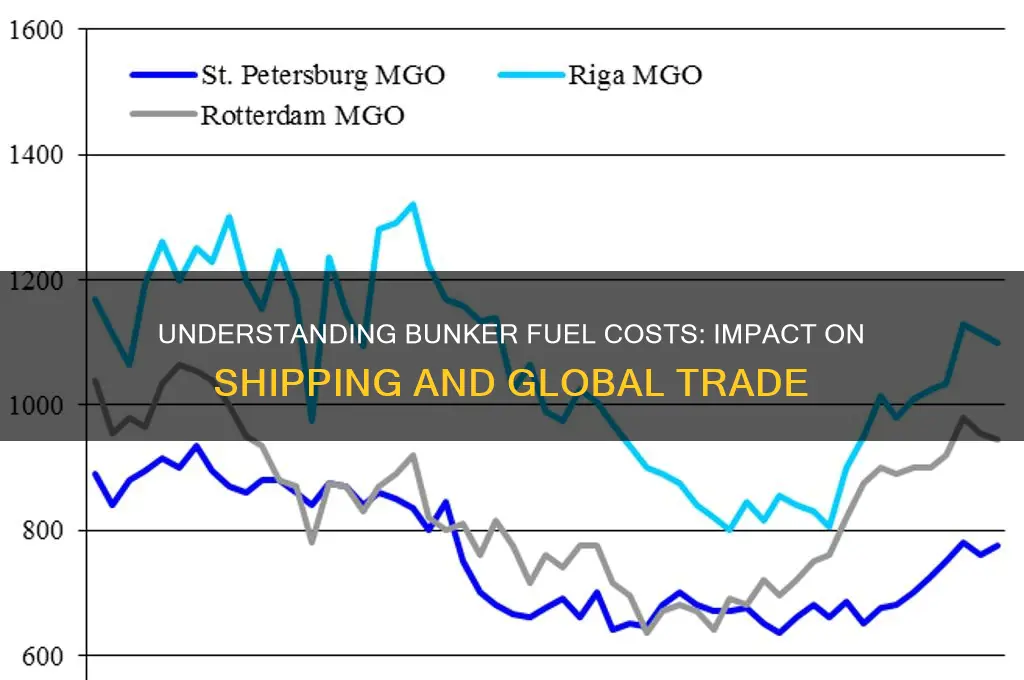

Regional Variations: How bunker fuel prices differ across major ports and shipping routes

Bunker fuel prices are not uniform across the globe; they fluctuate significantly depending on the region, port, and shipping route. This disparity is influenced by a myriad of factors, including local taxes, environmental regulations, supply and demand dynamics, and geopolitical tensions. For instance, ports in regions with stringent emissions regulations, such as the European Union or California, often see higher bunker fuel prices due to the need for low-sulfur fuels. Conversely, ports in regions with less stringent regulations, like parts of Asia or the Middle East, may offer cheaper bunker fuel but with higher sulfur content. Understanding these regional variations is crucial for shipping companies aiming to optimize operational costs and comply with international maritime regulations.

To illustrate, consider the price differences between Rotterdam, one of Europe’s largest ports, and Singapore, a major bunkering hub in Asia. As of recent data, Rotterdam’s bunker fuel prices are typically 10-15% higher than Singapore’s due to the EU’s stricter sulfur emission limits, which mandate the use of more expensive low-sulfur fuels. In contrast, Singapore benefits from its strategic location, robust supply chain, and competitive pricing, making it a preferred bunkering destination for many vessels traversing the Asia-Pacific region. Similarly, ports in the Middle East, such as Fujairah, often offer some of the lowest bunker fuel prices globally due to their proximity to oil production sites and lower operational costs.

Shipping routes also play a pivotal role in determining bunker fuel costs. For example, vessels traveling through the Suez Canal or the Panama Canal may experience price spikes due to high demand and limited supply in these critical chokepoints. Additionally, routes passing through regions prone to geopolitical instability, such as the Gulf of Guinea or the Strait of Hormuz, often face higher fuel costs due to increased insurance premiums and security risks. Companies can mitigate these costs by strategically planning refueling stops in ports with lower prices, a practice known as "bunker arbitrage."

Environmental regulations further exacerbate regional price differences. The International Maritime Organization’s (IMO) global sulfur cap, which limits sulfur content in marine fuels to 0.5%, has led to a two-tier market: one for compliant low-sulfur fuels and another for cheaper, higher-sulfur alternatives in regions where enforcement is lax. For instance, while ports in the U.S. and Europe strictly enforce the sulfur cap, some ports in Africa or Southeast Asia may still allow higher-sulfur fuels, creating significant price disparities. Shipping companies must navigate these regulatory landscapes carefully to avoid penalties and ensure compliance.

In conclusion, regional variations in bunker fuel prices are a complex interplay of economic, regulatory, and geopolitical factors. By analyzing these differences and adopting strategic bunkering practices, shipping companies can reduce costs and enhance operational efficiency. For instance, leveraging real-time fuel price data platforms, such as those provided by Bunkerworld or Ship & Bunker, can help companies identify the most cost-effective ports for refueling. Additionally, investing in fuel-efficient technologies and exploring alternative fuels, such as liquefied natural gas (LNG), can provide long-term cost savings and environmental benefits. Ultimately, a nuanced understanding of regional bunker fuel dynamics is indispensable for navigating the challenges of modern maritime logistics.

Are Turboprops More Fuel Efficient Than Jets? Exploring the Facts

You may want to see also

Explore related products

![]()

Cost Management: Strategies for reducing bunker fuel expenses, such as hedging and slow steaming

Bunker fuel, a critical expense in maritime operations, accounts for up to 50-60% of a vessel’s total operating costs. Fluctuations in global oil prices, geopolitical tensions, and environmental regulations further exacerbate this financial burden. To mitigate these expenses, shipping companies must adopt strategic cost management practices. Two effective strategies—hedging and slow steaming—stand out for their ability to reduce bunker fuel costs while balancing operational efficiency.

Hedging: A Financial Shield Against Price Volatility

Hedging involves using financial instruments, such as futures contracts or options, to lock in fuel prices for future purchases. For instance, if a company anticipates a rise in bunker fuel prices, it can enter into a futures contract to buy fuel at the current rate, protecting itself from higher costs later. A 2022 case study of a major container shipping line revealed that hedging saved them approximately $15 million annually by stabilizing fuel costs during a period of oil price spikes. However, hedging requires careful analysis of market trends and a risk management framework to avoid potential losses if prices move unfavorably. Companies should allocate no more than 30-40% of their fuel needs to hedging contracts to maintain flexibility.

Slow Steaming: Trading Speed for Savings

Slow steaming, reducing a vessel’s speed to minimize fuel consumption, is a proven method to cut bunker fuel expenses. For every 1-knot reduction in speed, fuel consumption can decrease by 18-24%. A bulk carrier traveling at 12 knots instead of 15 knots can save up to $10,000 per day in fuel costs on a long-haul route. While this strategy extends voyage times, it is particularly effective for non-time-sensitive cargoes like dry bulk or crude oil. To implement slow steaming, ship operators should optimize voyage planning, ensuring schedules account for longer transit times. Additionally, vessels must undergo regular maintenance to ensure engines operate efficiently at lower speeds.

Combining Strategies for Maximum Impact

While hedging and slow steaming are powerful individually, their combined application can yield even greater savings. For example, a company can hedge 30% of its fuel needs to protect against price spikes while implementing slow steaming to reduce overall consumption. This dual approach not only lowers fuel costs but also enhances predictability in budgeting. However, success depends on continuous monitoring of market conditions and operational data. Advanced analytics tools can help identify optimal hedging windows and ideal slow steaming speeds for specific routes.

Cautions and Considerations

Despite their benefits, these strategies are not without challenges. Over-reliance on hedging can lead to financial losses if prices move unexpectedly, while slow steaming may strain customer relationships due to delayed deliveries. Companies must also consider environmental regulations, such as the International Maritime Organization’s (IMO) 2020 sulfur cap, which has increased the cost of compliant low-sulfur fuels. In such cases, investing in alternative fuels or energy-efficient technologies may complement these strategies. Regular reviews of fuel management policies are essential to adapt to evolving market dynamics and regulatory requirements.

By strategically employing hedging and slow steaming, shipping companies can navigate the volatile bunker fuel market with greater financial resilience. These approaches, when tailored to specific operational needs and market conditions, offer a sustainable path to reducing fuel expenses without compromising long-term viability.

Understanding the Fuel Rail: Functions, Issues, and Maintenance Tips

You may want to see also

Explore related products

![]()

Environmental Impact: How emissions regulations and carbon taxes affect bunker fuel costs

Emissions regulations and carbon taxes are reshaping the bunker fuel market, forcing shipowners and operators to rethink their fuel strategies. The International Maritime Organization’s (IMO) 2020 sulfur cap, which reduced allowable sulfur content in marine fuels from 3.5% to 0.5%, immediately drove up costs for compliant low-sulfur fuels. For instance, the price differential between high-sulfur fuel oil (HSFO) and very low sulfur fuel oil (VLSFO) peaked at over $300 per metric ton in 2020. This regulatory shift not only increased operational expenses but also spurred investment in alternative fuels like liquefied natural gas (LNG) and scrubbers, which allow continued use of cheaper HSFO. However, these alternatives come with their own cost implications, such as the $2–4 million price tag for installing a scrubber system.

Carbon taxes are the next frontier in emissions regulation, adding another layer of complexity to bunker fuel costs. The European Union’s Emissions Trading System (EU ETS), which includes maritime emissions starting in 2024, will require ships to purchase allowances for each ton of CO₂ emitted. Analysts estimate this could add $50–$150 to the cost of a ton of fuel, depending on carbon prices. For a large container ship consuming 200 tons of fuel daily, this translates to an additional $10,000–$30,000 in daily operating costs. Such financial pressures are accelerating the transition to greener fuels like biofuels and ammonia, though these remain more expensive and less widely available than traditional bunker fuels.

The interplay between regulations and market dynamics is creating a bifurcated fuel landscape. While some operators opt for compliance through cleaner fuels, others are strategically routing vessels outside regulated zones to avoid higher costs. For example, ships traveling between Asia and Europe may detour around EU waters to burn cheaper, non-compliant fuels. However, this practice is increasingly risky as more regions adopt similar regulations. The IMO’s Carbon Intensity Indicator (CII) and Energy Efficiency Existing Ship Index (EEXI) further incentivize efficiency improvements, pushing operators to invest in hull coatings, propeller upgrades, and slow steaming—measures that reduce fuel consumption but require upfront capital.

Practical tips for navigating this regulatory environment include conducting a cost-benefit analysis of scrubbers versus low-sulfur fuels, monitoring carbon credit markets to hedge against price volatility, and exploring charter party clauses that allocate fuel cost increases between owners and charterers. Additionally, blending fuels or using LNG can provide short-term cost savings, though long-term sustainability goals may necessitate a shift to zero-emission technologies. As regulations tighten, staying informed and proactive is essential to minimizing bunker fuel costs while meeting environmental mandates.

Do Dunkin Points Have a Limit? Maximizing Your Rewards

You may want to see also

Frequently asked questions

Bunker fuel costs refer to the expenses incurred by ships for purchasing and using heavy fuel oil (HFO) or marine diesel oil (MDO) to power their engines during voyages. These costs are a significant component of a vessel's operational expenses.

Bunker fuel costs are influenced by factors such as global oil prices, supply and demand dynamics, geopolitical events, seasonal variations, and compliance with environmental regulations (e.g., low-sulfur fuel requirements under IMO 2020).

Bunker fuel costs directly affect shipping companies' profitability, as they account for a large portion of operational expenses. Fluctuations in fuel prices can lead to increased freight rates, altered trade routes, and investments in fuel-efficient technologies or alternative fuels.