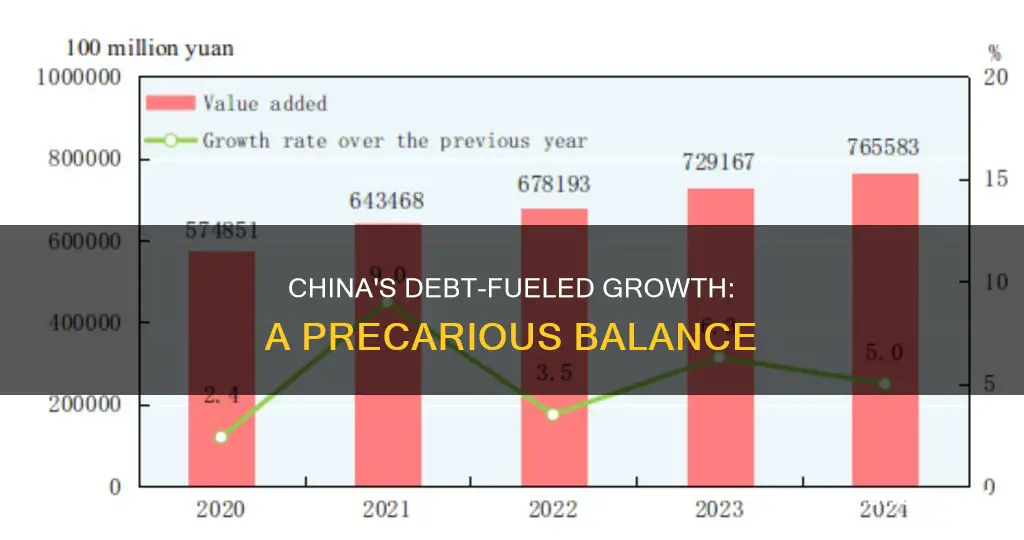

China's economic growth has been fuelled by debt, particularly after the 2008 financial crisis. The country's debt-to-GDP ratio has been rising rapidly, reaching 255.7% in 2017, one of the fastest rises in global history. This has been driven by the property sector, which has accounted for 23-30% of the economy, and large-scale infrastructure construction. The rapid expansion of the property sector was funded by household savings, with money flowing into risky property projects. China's high corporate debt is also a concern, with firms increasingly using loans to finance assets and taking on more risk. The country's stimulus packages, such as the $600 billion package in 2008, have contributed to the rise in debt, which has become a challenge for the Chinese Communist Party.

| Characteristics | Values |

|---|---|

| China's ranking in the world economy | Second-largest economy, after the US |

| China's debt in 2023 | $2.38 trillion |

| Local government debt in 2023 | 92 trillion yuan ($12.58 trillion) |

| China's credit growth projection for 2021 | 10% to 10.5% |

| China's credit growth in 2020 | 13.3% |

| China's debt-to-GDP ratio in 2017 | 255.7% |

| China's corporate debt | Steadily rising since the financial crisis |

| China's household debt in 2017 | 48.4% of GDP |

| China's trade surplus in 2024 | $992 billion (5.6% of China's GDP) |

| China's investment in property development after the collapse of the housing sector in 2022 | Declined rapidly |

| China's debt purpose | Funding large-scale infrastructure construction and urbanization |

Explore related products

What You'll Learn

![]()

China's rapid urbanization and construction

China's rapid urbanization has resulted in a massive increase in its urban population, with numbers rising from 172 million in 1978 to 749 million in 2014, surpassing 50% of the total population. This urbanization has been characterized by crowded living conditions but a notable absence of slums, indicating a level of success for a developing country. China has also managed to contain migration to villages or channel it to smaller cities, preventing the formation of slums. The hukou, or household registration system, has played a crucial role in controlling migration and directing it towards smaller cities.

Another key element of China's urbanization is the devolution of public services and administrative functions to city governments, which has led to increased satisfaction among citizens. China has also been mindful of its land use, with cities occupying only about 4.4% of the total land area. However, the rapid urbanization has resulted in various social and environmental problems, including rising income inequality and an impact on climate change and carbon emissions.

China's debt-fuelled growth has helped it become the world's second-largest economy, but it now faces challenges in reducing its reliance on debt. The COVID-19 pandemic further exacerbated the issue, with China's debt reaching record levels in 2020. Beijing has recognized the potential threat of this ballooning debt to its economic stability and is taking steps to address the issue.

Fuel Efficiency: Understanding Miles Per Gallon

You may want to see also

Explore related products

![]()

Government stimulus and credit expansion

China's rapid economic growth and urban development after the 2008 financial crisis were driven in part by booming credit. The country's debt levels stabilized for several years before reaching an all-time high of nearly 290% of gross domestic product (GDP) in the third quarter of 2020, according to the Bank of International Settlements. This dramatic rise in debt was a consequence of China's strategy of using turbo-charged stimulus financing to maintain moderate growth.

The Chinese government's stimulus was largely funded through loans from the state banking system, which contributed to an increase in debt that became unevenly distributed across industries and regions. China's credit boom led many firms to produce more goods than market conditions demanded, resulting in widespread overcapacity in 2018. The country's high level of corporate debt is a concern, as Chinese corporate leverage has steadily risen since the financial crisis, indicating that firms are increasingly using loans to finance assets and taking on more risk.

The main purpose of Chinese debt has been to fund large-scale infrastructure construction and urbanization, primarily through the use of local government financing vehicles (LGFV) that issue corporate bonds known as "urban construction and investment bonds" or "chengtou bonds". Local governments use land as collateral and borrow heavily from banks to promote urbanization and property development. Well-connected property developers purchase land at favourable rates from local governments and invest in infrastructure, benefiting local economies. Local governments also profit from land sales and tax revenues from construction and other business activities from new property development.

China's rapid urbanization and frenzied construction were largely funded by household savings, with household depositors parking their lifetime savings at Chinese banks and retail investors buying sophisticated wealth management products that promised high returns. However, in recent years, these investments have started generating negative returns as the money flows have slowed down, exposing the vulnerabilities of China's debt-fueled growth model.

Lucrative Fuel Hauling: How Much Can You Earn?

You may want to see also

Explore related products

![]()

The role of local government financing vehicles

Local government financing vehicles (LGFVs) have played a significant role in China's debt-fuelled growth. LGFVs are investment companies that borrow money from banks or by selling bonds in the open market to finance real estate development and local infrastructure projects. Since local governments in China are not authorised to issue municipal bonds, LGFVs have been instrumental in securing funding for local governments to develop their economies.

LGFVs issue corporate bonds known as "urban construction and investment bonds" or "chengtou bonds". These bonds have been a significant source of funding for large-scale infrastructure construction and urbanization projects in China. The revenue generated from these projects has contributed to the country's economic growth.

However, LGFVs rarely generate sufficient returns to repay their debts. As a result, local governments are often forced to raise additional funds to repay their creditors. The number of LGFVs and their indebtedness have increased significantly in recent years, raising concerns about their ability to service their debts and the potential risk of defaults.

To address these concerns, the Chinese government has implemented several measures. In 2019, LGFV bonds constituted 39% of total outstanding corporate bonds in China's domestic bond market. In 2021, new regulations prohibited financial institutions from providing additional liquidity to LGFVs, and local governments were required to raise funds through bond issuance, subject to stricter oversight. Despite these challenges, LGFVs continue to play a crucial role in China's economic development, and their management and restructuring remain a priority for the government.

In conclusion, LGFVs have been a double-edged sword in China's debt-fuelled growth. While they have provided essential funding for infrastructure development and urbanization, their reliance on debt and the potential risk of defaults have become a growing concern. The Chinese government and financial institutions are actively working to restructure and resolve LGFV debt to maintain economic stability and sustain China's remarkable growth trajectory.

Trucks' Fuel Tanks: Capacity and Consumption Explored

You may want to see also

Explore related products

$13.19 $26

![]()

Impact of the 2008 financial crisis

The 2008 financial crisis had a significant impact on China's economy, which was already experiencing rapid growth. The crisis originated in the United States in 2007 and led to the first contraction in global trade in 30 years. As a result, China's exports, which accounted for over 30% of its GDP and about one-third of its annual economic growth, collapsed in late 2008. The plunge in trade cut China's growth rate by about 3 percentage points in 2009 and by about 1 percentage point in the first quarter of 2010.

In response to the crisis, China implemented an aggressive fiscal policy and a loose monetary policy, which included a RMB 4 trillion ($580-586 billion) stimulus package for 2009 and 2010, announced in November 2008. This stimulus package aimed to minimize the impact of the Great Recession and was seen as a success, helping China avert a recession. While China's economic growth fell to almost 6% by the end of 2008, it recovered to over 10% by mid-2009. The stimulus package provided funds for infrastructure projects, housing developments, and social welfare plans, which expanded employment in various sectors.

However, the stimulus package also contributed to a surge in Chinese debt, particularly among local governments and state-owned enterprises. Bank lending in China totaled RMB 9.6 trillion in 2009, reaching nearly half of that year's GDP. While China's debt-to-GDP ratio remained relatively low at the end of 2009, the rapid increase in debt has been a concern for the country in the years following the financial crisis.

The global financial crisis had a devastating effect on the world economy, wiping out the strong growth posted by most economies in 2007 and early 2008. China's economy was no exception, as it experienced a downward spiral due to plunging world demand. However, as the world economy began to stabilize in 2009 and the stimulus package took effect, China's economic situation improved.

In conclusion, the 2008 financial crisis impacted China's economy significantly, leading to a collapse in exports and a slowdown in growth. China's response included an aggressive stimulus package that helped avert a recession and contributed to a recovery in growth. However, it also led to an increase in the country's debt, which has become a challenge for China in subsequent years.

Ford Pinto Fuel Capacity: How Much Can It Hold?

You may want to see also

Explore related products

![]()

The property sector crisis

China's property sector crisis, sparked by the 2021 default of Evergrande Group, has had a significant impact on the country's economy. Evergrande, once the world's most valuable real estate company, collapsed due to excessive borrowing and overbuilding, with liabilities exceeding its assets. The crisis spread beyond Evergrande to other major property developers, including Country Garden, Kaisa Group, and Sunac, impacting global markets and leading to a slowdown of foreign investment in China.

The property sector has been a key driver of China's debt-fueled growth model in the past two decades, contributing between 23% and 30% of the economy. Local governments used land as collateral to secure loans from banks and promote urbanization and property development. Well-connected property developers purchased land at favourable rates and invested in local infrastructure, benefiting local economies. Local governments also profited from land sales and tax revenues from construction and other business activities.

However, the rapid expansion of the property sector was largely funded by household savings, with banks offering high-return investments that were channelled into risky property projects. When Xi Jinping imposed the "three red lines" policies, which constrained cheap loans to property developers, the flow of money slowed down, leading to a crisis in the property sector. The pandemic also hit China's economic growth, prompting authorities to ease lending requirements for companies, further contributing to the country's debt burden.

The Chinese government has implemented several measures to stimulate the housing market, including lowering down payment thresholds, reducing mortgage interest rates, and increasing bank lending. In March 2024, China's minister of housing and urban-rural development, Ni Hong, acknowledged the severity of the crisis and stated that real estate developers must go bankrupt if necessary. Despite these efforts, the future of China's real estate market remains uncertain, and the crisis has highlighted the challenges of transitioning from a real-estate-led growth model to more balanced growth.

The High Cost of Rocket Fuel: How Much Does it Burn?

You may want to see also

Frequently asked questions

China's rapid urbanization and construction have been funded by ordinary people, such as household depositors and retail investors. This has resulted in a win-win situation for local governments, property developers, and local economies.

China's debt has grown rapidly over the past decade, especially after the 2008 financial crisis. In 2017, China's total debt was 255.7% of its GDP, with a credit-to-GDP growth of 48.4% between 2012 and 2017. In 2020, China's debt-to-GDP ratio reached an all-time high of nearly 290%.

There are concerns about the rate of China's debt growth and its impact on economic stability. China's high corporate debt and over-reliance on debt-fueled investment have contributed to growing financial vulnerabilities. The collapse of the housing sector in 2022 and the property sector crisis have further impacted China's economy.