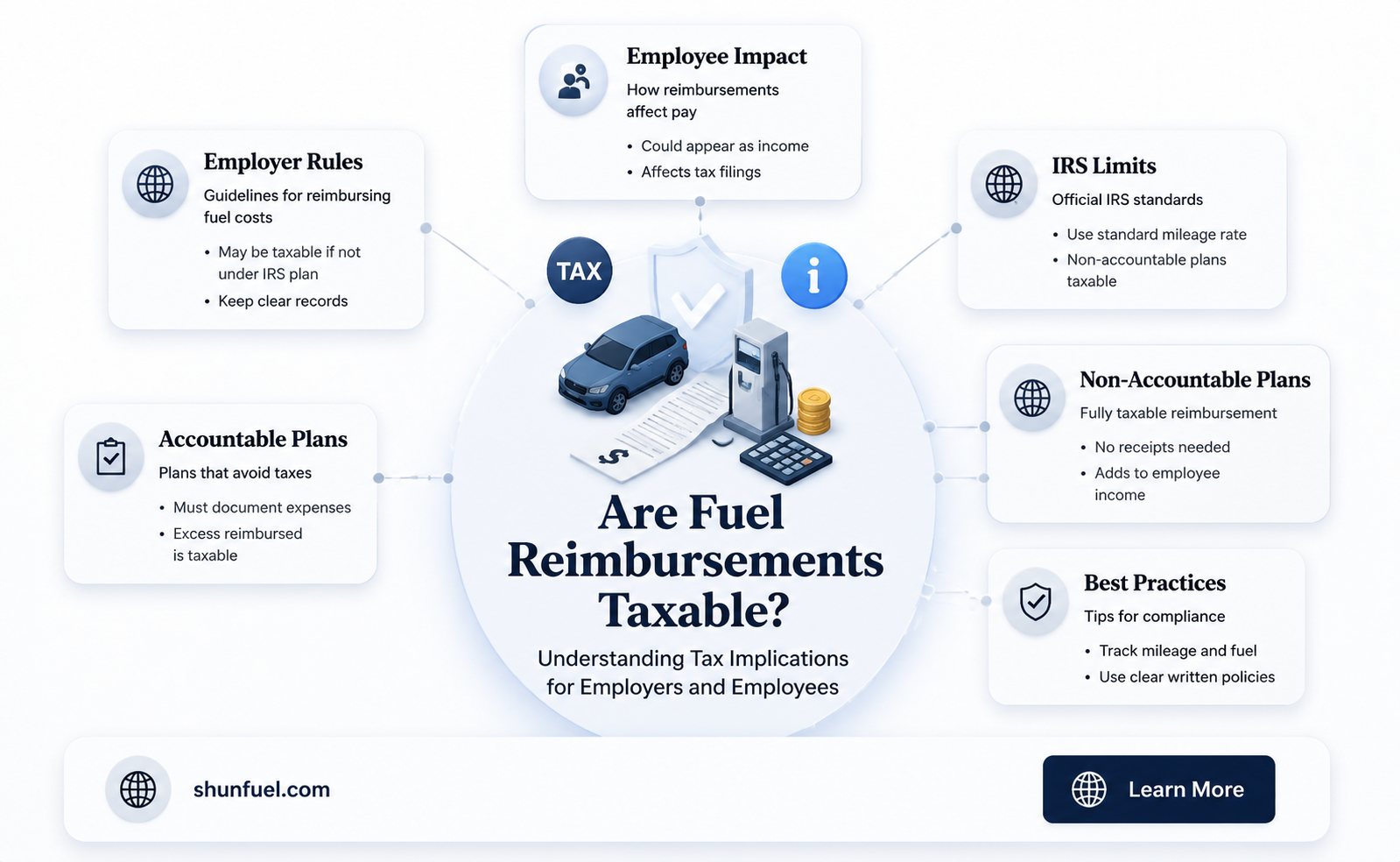

Fuel reimbursements can be a complex topic when it comes to taxation, as their taxability often depends on the specific circumstances under which they are provided. Generally, if an employer reimburses an employee for fuel expenses incurred while performing job-related duties, these reimbursements may be considered non-taxable if they meet certain criteria, such as being part of an accountable plan. Under an accountable plan, employees must substantiate their expenses with proper documentation and return any excess reimbursements. However, if the reimbursements are provided as a fixed allowance or do not meet the requirements of an accountable plan, they may be treated as taxable income, subject to federal income tax and payroll taxes. Understanding the nuances of these rules is crucial for both employers and employees to ensure compliance with tax regulations and avoid potential penalties.

| Characteristics | Values |

|---|---|

| Taxability of Fuel Reimbursements | Depends on the method used (accountable plan vs. non-accountable plan). |

| Accountable Plan | Reimbursements are tax-free for both employer and employee. |

| Requirements for Accountable Plan | 1. Business connection. 2. Adequate accounting (receipts, records). 3. Excess returns. |

| Non-Accountable Plan | Reimbursements are taxable as income to the employee. |

| IRS Mileage Rate (2023) | 65.5 cents per mile (business miles); reimbursements up to this rate are tax-free if using an accountable plan. |

| Fixed and Variable Rate Reimbursement (FAVR) | Tax-free if meets IRS criteria for accountable plans. |

| Tax Reporting | Accountable plans: Not reported on W-2. Non-accountable plans: Reported as wages on W-2. |

| State Tax Treatment | Varies by state; some states follow federal rules, others may differ. |

| Documentation Required | Detailed mileage logs, receipts, and purpose of travel for accountable plans. |

| Employer Deduction | Reimbursements under accountable plans are deductible as business expenses. |

| Employee Deduction (if taxable) | May be deductible as an unreimbursed business expense (subject to 2% AGI floor). |

Explore related products

What You'll Learn

![]()

IRS Rules on Fuel Reimbursements

Fuel reimbursements can be a tax-free benefit for employees, but only if they meet specific IRS criteria. The IRS allows tax-exempt reimbursements under an accountable plan, which requires detailed record-keeping and substantiation. Employees must provide evidence of business mileage, such as a mileage log, and the reimbursement rate cannot exceed the standard mileage rate set by the IRS (currently 65.5 cents per mile for 2023). If these conditions are met, the reimbursement is not considered taxable income for the employee and is not subject to payroll taxes for the employer.

To implement an accountable plan, employers must follow a structured process. First, employees should track business miles driven using a log that includes dates, destinations, and purposes. Second, reimbursements must be paid only for miles driven for business purposes, excluding commuting miles. Third, any excess payments must be returned to the employer within a reasonable time frame. Failure to adhere to these rules can result in the reimbursement being treated as taxable wages, subject to income tax and payroll tax withholding.

A common mistake is using a fixed allowance or flat-rate reimbursement without proper substantiation. For example, providing a monthly car allowance without requiring mileage logs violates IRS rules, making the payments taxable. In contrast, reimbursing employees based on actual business miles driven, supported by documentation, aligns with IRS guidelines and remains tax-free. This distinction highlights the importance of tying reimbursements directly to business expenses rather than providing a general stipend.

For employers, understanding these rules is crucial for compliance and cost management. Tax-free reimbursements reduce payroll tax liabilities, while taxable reimbursements increase them. Employees benefit from tax-free reimbursements as they receive the full amount without reduction for taxes. However, both parties must stay updated on IRS mileage rates and regulations, as these can change annually. For instance, the 2023 rate of 65.5 cents per mile reflects an increase from previous years due to rising fuel costs.

In summary, fuel reimbursements can be tax-free under an accountable plan, but strict adherence to IRS rules is essential. Employers should require detailed mileage logs, ensure reimbursements are based on actual business use, and avoid flat allowances. Employees must maintain accurate records to substantiate their claims. By following these guidelines, both parties can maximize tax benefits while remaining compliant with IRS regulations.

Mastering Fuel Surcharge Calculations: A Step-by-Step Guide for Businesses

You may want to see also

Explore related products

![]()

Accountable vs. Non-Accountable Plans

Fuel reimbursements can be a tax-free benefit for employees, but the treatment depends on whether the employer uses an Accountable Plan or a Non-Accountable Plan. Understanding the distinction is critical for both employers and employees to ensure compliance with IRS regulations and maximize tax efficiency.

Accountable Plans are designed to reimburse employees for business-related expenses, including fuel, in a way that avoids taxable income for the employee. To qualify, the plan must meet three key IRS requirements: (1) expenses must have a clear business connection, (2) employees must adequately account for expenses within 60 days of incurring them, and (3) any excess reimbursements must be returned within 120 days. For example, if an employee submits fuel receipts totaling $200 for a work-related trip, the reimbursement is tax-free as long as the plan adheres to these rules. Employers benefit by deducting these reimbursements as business expenses, while employees avoid paying taxes on the funds.

In contrast, Non-Accountable Plans do not meet IRS requirements for tax-free treatment. Under these plans, reimbursements are treated as taxable wages, subject to income tax withholding and payroll taxes. For instance, if an employer provides a flat $100 monthly fuel allowance without requiring documentation or return of excess funds, this amount is taxable to the employee. While simpler to administer, this approach reduces the employee’s net pay and increases the employer’s payroll tax liability.

The choice between these plans often hinges on administrative feasibility and the level of control employers wish to maintain. Accountable Plans require more record-keeping but offer significant tax advantages. Non-Accountable Plans, while easier to manage, result in higher tax costs for both parties. For employers, implementing an Accountable Plan involves setting clear policies, providing timely reimbursement, and ensuring employees submit detailed expense reports. Employees, meanwhile, must retain receipts and adhere to deadlines to maintain tax-free status.

In practice, businesses should evaluate their operational needs and employee travel patterns before selecting a plan. For companies with frequent, well-documented business travel, an Accountable Plan is often the better choice. Conversely, businesses with minimal or inconsistent travel may find a Non-Accountable Plan more practical, despite the tax implications. Ultimately, the goal is to align the reimbursement structure with both IRS guidelines and organizational priorities, ensuring fairness and compliance for all involved.

Does Hawaiian Airlines Hedge Fuel Costs? A Comprehensive Analysis

You may want to see also

Explore related products

![]()

Taxable Fringe Benefits for Fuel

Fuel reimbursements can be a double-edged sword for employees and employers alike. While they provide financial relief for work-related travel, they often come with tax implications that are not immediately obvious. One critical area to understand is how these reimbursements fall under the category of taxable fringe benefits. Fringe benefits are non-cash perks provided by employers, and when they relate to fuel, they can trigger taxable events if not structured correctly.

Consider the IRS’s rules on accountable and non-accountable plans. An accountable plan allows employees to receive tax-free reimbursements for fuel expenses, provided they meet three criteria: the expenses must be business-related, substantiated with proper documentation, and any excess amounts must be returned to the employer. For example, if an employee drives 100 miles for work and submits a mileage log, the reimbursement at the IRS standard rate (65.5 cents per mile in 2023) is tax-free. However, if the employer provides a flat allowance without requiring documentation, it becomes a non-accountable plan, and the reimbursement is taxable as income.

The distinction between taxable and non-taxable fuel reimbursements hinges on accountability and documentation. Employers must ensure their reimbursement policies comply with IRS guidelines to avoid unintended tax liabilities for employees. For instance, using a fuel card that restricts purchases to gasoline and requires mileage logs can help maintain accountability. Conversely, providing a cash allowance without tracking usage can result in the entire amount being treated as taxable income, reducing the net benefit to the employee.

From a practical standpoint, employers should implement clear policies that align with IRS requirements. This includes educating employees on the importance of maintaining detailed records, such as mileage logs and receipts. Employees, on the other hand, should proactively track their fuel expenses to maximize tax-free reimbursements. For self-employed individuals, the rules differ slightly; they can deduct actual vehicle expenses or use the standard mileage rate, but proper documentation remains essential.

In summary, fuel reimbursements as fringe benefits are taxable unless they meet the criteria for an accountable plan. By understanding and adhering to IRS guidelines, both employers and employees can navigate this complex area effectively. Proper documentation and policy compliance are key to ensuring these benefits remain tax-efficient, providing real value without unexpected financial burdens.

Effective Methods to Safely Destroy Fuel: A Comprehensive Guide

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

Mileage Rate and Tax Implications

The IRS sets a standard mileage rate to simplify reimbursement for business-related driving, but this rate isn’t just a flat fee—it carries tax implications for both employers and employees. For 2023, the rate is 65.5 cents per mile for business travel, a figure that includes fuel, maintenance, depreciation, and insurance costs. While this rate is tax-free for employees if properly documented, reimbursements above this rate may be taxable as income. Employers must tread carefully: reimbursements below the standard rate could leave employees footing the bill for additional expenses, while overpayments risk triggering payroll taxes.

Consider a scenario where an employee drives 1,000 miles for work in a month. At the 2023 rate, they’d receive $655 tax-free. However, if the employer reimburses $700, the extra $45 becomes taxable income. Conversely, if the employer reimburses $600, the employee absorbs the $55 difference, which could lead to dissatisfaction or claims for additional deductions. The key is alignment with the IRS rate to ensure fairness and compliance. For employers, using the standard mileage rate eliminates the need to track actual expenses, streamlining accounting and reducing administrative burden.

From a tax perspective, the standard mileage rate acts as a safe harbor. Employers who reimburse at or below this rate can exclude the payments from employees’ taxable wages, provided the reimbursements are for legitimate business travel. Employees benefit by avoiding the hassle of itemizing car-related expenses, while employers avoid the complexity of substantiating each cost. However, this simplicity comes with a trade-off: the rate is a fixed average and may not reflect individual drivers’ actual costs, particularly for those with older vehicles or high maintenance needs.

Practical tips for navigating this system include maintaining detailed mileage logs, which are mandatory for tax-free reimbursements. Apps like MileIQ or Everlance can automate tracking, ensuring accuracy and saving time. Employers should communicate the reimbursement policy clearly, emphasizing that personal or commuting miles are ineligible. For those in states with higher fuel costs, consider supplementing the federal rate with a non-taxable allowance for fuel, provided it’s separately documented. Finally, consult a tax professional to tailor the approach to your organization’s needs, especially if employees frequently drive for work.

In conclusion, the mileage rate is a powerful tool for simplifying fuel reimbursements, but its tax implications demand precision. By adhering to the IRS rate, maintaining thorough records, and staying informed about updates, both employers and employees can navigate this terrain efficiently. Missteps can lead to unnecessary tax liabilities or employee dissatisfaction, but with careful planning, the system offers a win-win solution for managing work-related driving expenses.

Smart Fuel-Saving Tips: Debunking Myths and Maximizing Efficiency on the Road

You may want to see also

Explore related products

![TurboTax Desktop Deluxe 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71uOJaU7UvL._AC_UY218_.jpg)

![TurboTax Desktop Premier 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71RgxnEm-tL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![TurboTax Desktop Home & Business 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71KOcfYElCL._AC_UY218_.jpg)

![TurboTax Desktop Deluxe 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71zRbfw0RdL._AC_UY218_.jpg)

![]()

Reporting Reimbursements on Tax Returns

Fuel reimbursements can be a tax-free benefit for employees, but only if they meet specific IRS criteria. The key lies in whether the reimbursement is considered accountable or non-accountable. Accountable plans, which require detailed expense reporting and timely returns of excess funds, allow reimbursements to remain tax-free for both the employer and employee. Non-accountable plans, lacking these controls, treat reimbursements as taxable income, subjecting them to payroll taxes and income tax withholding.

To report reimbursements correctly, employees must understand their plan type. For accountable plans, no reporting is required on the employee’s tax return, as the reimbursements are not considered income. Employers, however, must ensure their plan meets IRS standards: expenses must be business-related, substantiated with receipts, and any excess returned within 120 days. Failure to meet these criteria can reclassify the plan as non-accountable, triggering tax liabilities.

When reimbursements are taxable, employees report them as wages on Form W-2. This includes mileage reimbursements that exceed the IRS standard mileage rate or cover personal expenses. For example, if an employee receives $0.65 per mile but the IRS rate is $0.63, the $0.02 difference per mile is taxable. Employers must calculate and withhold taxes on this amount, while employees should account for it when filing their returns.

Self-employed individuals face a different scenario. They deduct actual vehicle expenses or use the standard mileage rate on Schedule C, but reimbursements received (e.g., from clients) reduce their deductible expenses. For instance, if a self-employed worker drives 10,000 business miles and receives $5,000 in reimbursements, they can claim only $1,000 ($0.63/mile × 10,000 - $5,000) as a deduction. Proper record-keeping is critical to avoid overstating deductions or underreporting income.

Practical tips include maintaining detailed mileage logs, retaining receipts for all expenses, and regularly reviewing IRS guidelines for updates. Employers should clearly communicate plan rules to employees and ensure compliance to avoid audits. Employees should verify their W-2 for accuracy and consult a tax professional if unsure about reporting taxable reimbursements. By staying organized and informed, both parties can navigate fuel reimbursement taxation efficiently.

Easy Guide to Filling Fuel in Your Zipcar Rental Vehicle

You may want to see also

Frequently asked questions

Fuel reimbursements are taxable if they exceed the IRS standard mileage rate or are not properly accounted for under an accountable plan.

Fuel reimbursements are non-taxable if they are part of an accountable plan, where employees provide adequate documentation of business mileage and expenses.

Yes, fuel reimbursements that exceed actual business expenses or are not part of an accountable plan are considered taxable income.

Employers can reimburse employees tax-free if the reimbursements are based on the IRS standard mileage rate or are part of an accountable plan with proper documentation.

Fixed-rate reimbursements up to the IRS standard mileage rate are generally tax-free, but amounts exceeding this rate may be taxable unless properly accounted for.

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)

![TurboTax Desktop Business 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71UL+5xLOeL._AC_UY218_.jpg)