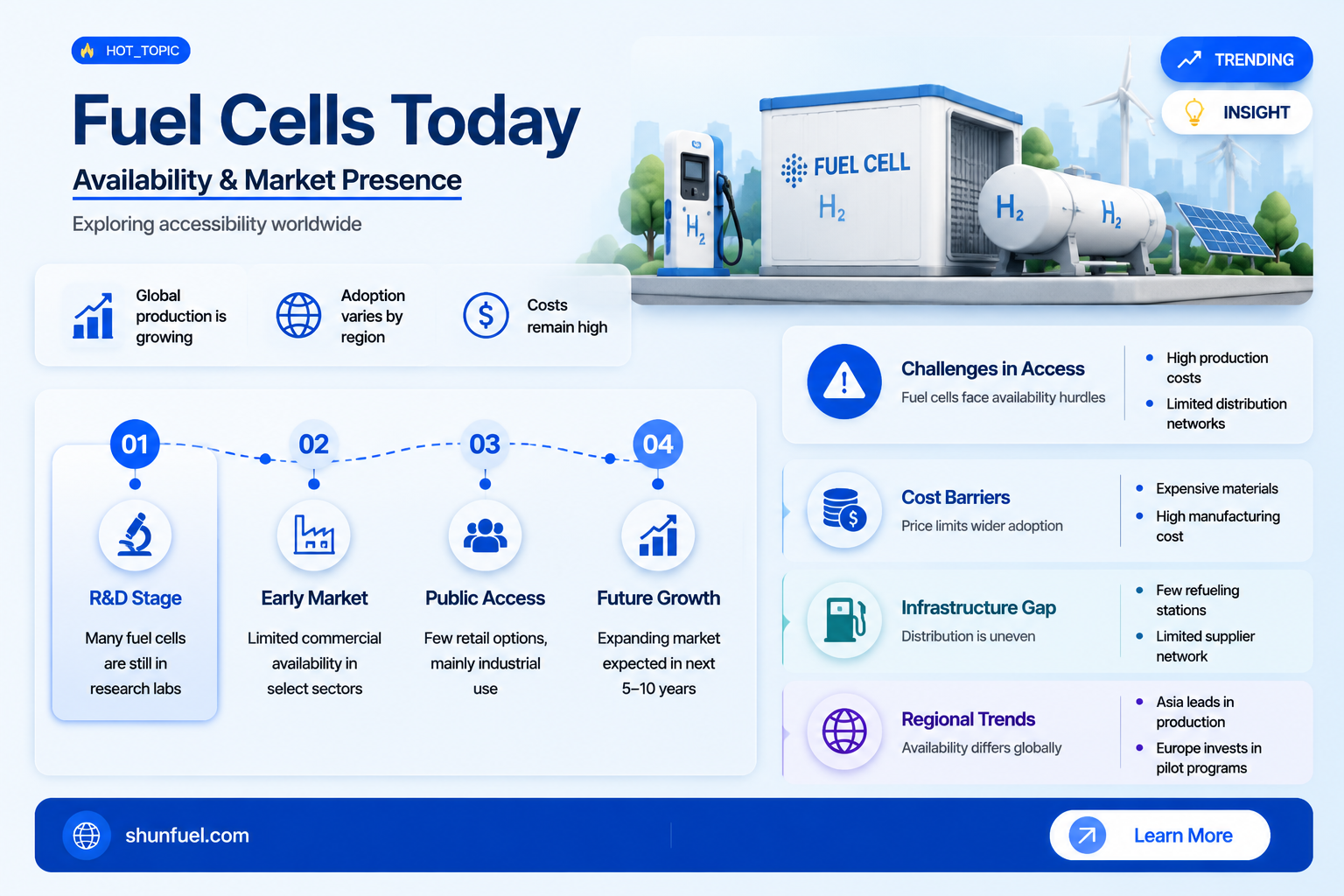

Fuel cells, which generate electricity through a chemical reaction between hydrogen and oxygen, have been a topic of interest for decades due to their potential as a clean and efficient energy source. While significant advancements have been made in fuel cell technology, their widespread availability remains limited. Currently, fuel cells are primarily used in niche applications such as material handling equipment, backup power systems, and certain vehicle models, particularly in regions with supportive infrastructure like Japan, California, and parts of Europe. However, challenges such as high production costs, limited hydrogen refueling stations, and competition from battery-electric technologies have hindered their broader adoption. As a result, while fuel cells are available in specific markets and industries, they are not yet readily accessible to the general public on a large scale.

| Characteristics | Values |

|---|---|

| Commercial Availability | Yes, fuel cells are commercially available for various applications. |

| Market Maturity | Growing, with increasing adoption in transportation, stationary power, and portable devices. |

| Cost | Decreasing, but still higher than traditional combustion engines or batteries. |

| Types Available | Proton Exchange Membrane (PEM), Solid Oxide Fuel Cells (SOFC), Alkaline, etc. |

| Applications | Vehicles (e.g., hydrogen fuel cell cars), backup power systems, material handling equipment, and portable electronics. |

| Infrastructure | Limited hydrogen refueling stations globally, but expanding in regions like Europe, Japan, and California. |

| Manufacturers | Toyota, Hyundai, Ballard Power Systems, Plug Power, and others. |

| Environmental Impact | Zero direct emissions (water and heat as byproducts), but depends on hydrogen production method. |

| Efficiency | High efficiency (40-60%), especially in combined heat and power (CHP) systems. |

| Durability | Improving, with lifespans comparable to traditional engines in some applications. |

| Government Support | Significant incentives and subsidies in many countries to promote adoption. |

| Challenges | High initial costs, limited infrastructure, and dependence on clean hydrogen production. |

| Future Outlook | Expected to grow with advancements in technology and infrastructure development. |

Explore related products

$159.99 $179.99

What You'll Learn

- Current market availability of fuel cell vehicles and their accessibility to consumers

- Distribution networks for fuel cell technology in different regions globally

- Challenges in producing and supplying hydrogen fuel for cell operations

- Cost barriers limiting widespread adoption of fuel cell technology

- Government policies and incentives supporting fuel cell infrastructure development

![]()

Current market availability of fuel cell vehicles and their accessibility to consumers

Fuel cell vehicles (FCVs) are no longer a futuristic concept but a tangible, if still niche, option in the automotive market. As of recent data, major manufacturers like Toyota, Hyundai, and Honda have introduced models such as the Toyota Mirai, Hyundai Nexo, and Honda Clarity, making FCVs commercially available in select regions. However, their presence remains limited, primarily due to high production costs and a lack of widespread hydrogen refueling infrastructure. For instance, in the United States, FCVs are predominantly found in California, where 53 hydrogen stations support their operation, compared to thousands of electric vehicle charging stations nationwide.

The accessibility of fuel cell vehicles to consumers hinges on geographic location and financial considerations. In markets like Japan, South Korea, and parts of Europe, government incentives and investments in hydrogen infrastructure have made FCVs more viable. For example, Japan aims to have 800,000 FCVs on the road by 2030, supported by subsidies and a growing network of refueling stations. Conversely, in regions without such support, the high purchase price of FCVs—often $5,000 to $10,000 more than comparable electric vehicles—and the scarcity of refueling options create significant barriers for average consumers.

From a practical standpoint, owning a fuel cell vehicle requires careful planning. Prospective buyers should first verify the availability of hydrogen stations within their daily driving radius, as the current infrastructure is sparse outside of major metropolitan areas. Additionally, leasing is often a more accessible option than purchasing, with some manufacturers offering lease deals that include hydrogen fuel allowances. For instance, Toyota’s Mirai lease in California starts at around $450 per month, with $15,000 due at signing, and includes up to $15,000 in fuel credits over three years.

Comparatively, fuel cell vehicles offer advantages over battery electric vehicles (BEVs) in terms of refueling time and range, with most FCVs filling up in under five minutes and achieving ranges of 300–400 miles. However, BEVs benefit from a more established charging network and lower overall costs, making them the more accessible choice for most consumers. The takeaway is that while FCVs are available, their accessibility remains constrained by infrastructure limitations and higher costs, positioning them as a specialized option rather than a mainstream solution.

To enhance accessibility, policymakers and industry stakeholders must prioritize expanding hydrogen infrastructure and reducing production costs. Initiatives like the European Union’s Hydrogen Strategy and California’s goal of 200 hydrogen stations by 2025 are steps in the right direction. Consumers interested in FCVs should stay informed about local incentives and infrastructure developments, as these factors will determine whether fuel cell vehicles become a practical choice in their area. For now, FCVs represent a promising but niche segment of the automotive market, accessible primarily to early adopters in well-supported regions.

EPA Fuel Economy Testing: Methods, Accuracy, and Real-World Implications

You may want to see also

Explore related products

![]()

Distribution networks for fuel cell technology in different regions globally

Fuel cell technology, while not yet ubiquitous, is gaining traction globally, with distribution networks emerging to support its adoption. In North America, particularly the United States, initiatives like the Hydrogen and Fuel Cell Technologies Office (HFTO) under the Department of Energy have spurred the development of refueling stations, primarily in California. As of 2023, California alone boasts over 50 hydrogen refueling stations, a critical step in making fuel cell vehicles (FCEVs) viable for consumers. However, the rest of the U.S. lags, with only a handful of stations in states like New York and Hawaii, highlighting the uneven distribution of infrastructure.

In contrast, Japan has taken a more holistic approach, integrating fuel cell technology into both transportation and stationary power systems. The country’s hydrogen roadmap, led by the Ministry of Economy, Trade, and Industry (METI), aims to establish 900 hydrogen refueling stations by 2030. Toyota’s Mirai FCEV and stationary fuel cell systems like ENE-FARM are prime examples of how Japan’s distribution networks are designed to cater to both mobility and residential energy needs. This dual focus ensures broader market penetration and consumer acceptance.

Europe’s distribution networks for fuel cell technology are fragmented but ambitious, with Germany and the Netherlands leading the charge. Germany’s H2 Mobility initiative plans to expand its network to 400 hydrogen stations by 2030, while the Netherlands focuses on integrating fuel cells into public transport, such as buses and trains. The European Union’s Hydrogen Strategy further supports cross-border collaboration, aiming to create a unified hydrogen market. However, the region’s progress is hindered by varying national policies and slower consumer adoption compared to Asia.

In Asia, beyond Japan, China is rapidly scaling its fuel cell distribution networks, particularly for commercial vehicles like trucks and buses. The government’s subsidies and mandates for hydrogen-powered fleets have accelerated infrastructure development, with over 200 refueling stations operational as of 2023. South Korea, meanwhile, is focusing on urban applications, deploying fuel cell taxis and buses in cities like Seoul. These regional strategies reflect a tailored approach to addressing local energy demands and environmental goals.

For regions looking to establish or expand fuel cell distribution networks, several key steps are essential. First, secure public-private partnerships to fund infrastructure development, as seen in Japan’s METI collaborations. Second, prioritize high-demand areas like urban centers or transportation corridors to maximize utilization. Third, integrate fuel cell technology into existing energy systems, such as combining hydrogen refueling with renewable energy production. Cautions include avoiding over-reliance on government subsidies, ensuring safety standards for hydrogen storage and transport, and addressing public skepticism through education campaigns. By learning from global examples, regions can build effective distribution networks that make fuel cell technology readily available and sustainable.

Synthetic Fuel Distribution: Revolutionizing Energy Supply Chains Globally

You may want to see also

Explore related products

![]()

Challenges in producing and supplying hydrogen fuel for cell operations

Hydrogen fuel cells are hailed as a clean energy solution, but their widespread adoption hinges on overcoming significant hurdles in hydrogen production and supply. The primary challenge lies in the energy-intensive nature of hydrogen extraction. Most hydrogen today is produced through steam methane reforming, a process that releases substantial carbon dioxide, undermining the environmental benefits of fuel cells. While electrolysis offers a greener alternative by splitting water into hydrogen and oxygen using electricity, it demands a reliable and renewable power source to be truly sustainable. Without a shift to low-carbon production methods, hydrogen fuel cells risk perpetuating the very emissions they aim to eliminate.

Scaling up hydrogen infrastructure presents another formidable obstacle. Unlike gasoline or diesel, hydrogen requires specialized storage and distribution networks. High-pressure tanks, cryogenic facilities, and pipelines designed to handle hydrogen’s unique properties are costly to build and maintain. For instance, hydrogen’s low density necessitates storage at pressures of up to 700 bar or temperatures near absolute zero, adding complexity and expense. Moreover, the lack of a widespread refueling network limits the practicality of hydrogen-powered vehicles, creating a chicken-and-egg scenario where consumers hesitate to adopt fuel cell vehicles due to insufficient infrastructure, and investors shy away from building infrastructure without a critical mass of users.

The economic viability of hydrogen production and supply further complicates its readiness. Green hydrogen, produced via electrolysis powered by renewable energy, is currently two to three times more expensive than its fossil fuel-derived counterpart. While costs are projected to decline as technology advances and renewable energy becomes cheaper, achieving price parity remains years away. Governments and private sectors must collaborate to fund research, subsidize production, and incentivize adoption. For example, the European Union’s Hydrogen Strategy aims to install 40 GW of electrolyzers by 2030, but such initiatives require sustained political will and financial commitment.

Finally, safety concerns and public perception pose subtle yet significant challenges. Hydrogen’s highly flammable nature demands stringent safety protocols in production, storage, and transportation. While hydrogen is no more dangerous than other fuels when handled properly, incidents like the 2019 Norway hydrogen station fire can fuel public skepticism. Education campaigns and transparent communication about safety measures are essential to build trust. Additionally, integrating hydrogen into existing energy systems requires regulatory frameworks that address liability, standards, and interoperability, ensuring seamless adoption without compromising safety or efficiency.

In summary, while hydrogen fuel cells hold immense potential, their availability is constrained by production inefficiencies, infrastructure gaps, economic barriers, and safety concerns. Addressing these challenges requires a multifaceted approach, combining technological innovation, strategic investment, and policy support. Until these hurdles are cleared, the promise of hydrogen as a readily available fuel source will remain largely theoretical.

Understanding the Process: How HOB Fuel is Manufactured and Utilized

You may want to see also

Explore related products

$114.99

![]()

Cost barriers limiting widespread adoption of fuel cell technology

Fuel cells, despite their promise as a clean and efficient energy source, remain largely inaccessible to the average consumer due to prohibitive costs. The primary expense lies in the materials used to construct fuel cells, particularly platinum, which serves as a catalyst in many designs. A single fuel cell vehicle, for instance, can require up to 30 grams of platinum, valued at over $1,000 at current market prices. This material cost alone dwarfs the expense of traditional internal combustion engine components, creating a significant barrier to entry for manufacturers and consumers alike.

To illustrate the financial challenge, consider the production of hydrogen fuel cell electric vehicles (FCEVs). While companies like Toyota and Hyundai have made strides with models such as the Mirai and Nexo, these vehicles often carry price tags exceeding $50,000, compared to $30,000–$40,000 for comparable battery electric vehicles (BEVs). The higher cost is not merely due to platinum but also stems from the complexity of fuel cell systems, which require precise engineering to manage hydrogen storage, compression, and conversion into electricity. These technical demands drive up manufacturing and research expenses, which are ultimately passed on to consumers.

Another critical cost barrier is the lack of infrastructure for hydrogen refueling. Building a single hydrogen refueling station can cost between $1 million and $2 million, compared to the relatively modest expense of installing electric vehicle charging stations. This disparity limits the practicality of FCEVs, as consumers are hesitant to invest in vehicles without convenient access to fuel. Governments and private companies face a chicken-and-egg dilemma: without widespread adoption of FCEVs, there is little incentive to invest in refueling infrastructure, and without infrastructure, FCEVs remain unappealing to buyers.

Despite these challenges, there are pathways to reduce costs and accelerate adoption. Research into alternative catalysts, such as iron-nitrogen-carbon compounds, could significantly lower material expenses. Economies of scale in manufacturing, coupled with policy incentives like tax credits or subsidies, could also make fuel cell technology more affordable. For instance, California’s Hydrogen Fuel Cell Partnership has invested heavily in both vehicles and infrastructure, demonstrating how targeted initiatives can bridge the cost gap. While fuel cells are not yet readily available to the masses, strategic investments and innovations could pave the way for broader accessibility in the future.

Fuel Injection vs Carburetors: Understanding the Key Differences

You may want to see also

Explore related products

![]()

Government policies and incentives supporting fuel cell infrastructure development

Governments worldwide are increasingly recognizing the critical role of fuel cell technology in achieving sustainability goals, particularly in reducing greenhouse gas emissions and enhancing energy security. To accelerate the adoption of fuel cells, policymakers have implemented a range of targeted incentives and regulations. For instance, the United States’ Inflation Reduction Act of 2022 includes tax credits for hydrogen production and fuel cell infrastructure, while the European Union’s Green Deal prioritizes hydrogen as a key component of its decarbonization strategy. These policies not only reduce the financial barriers to entry but also signal long-term commitment to stakeholders, fostering investment in research, development, and deployment.

One of the most effective strategies governments employ is the establishment of grants and subsidies for fuel cell projects. In Japan, the Ministry of Economy, Trade, and Industry (METI) offers substantial funding for hydrogen refueling stations and fuel cell vehicle (FCV) manufacturing. Similarly, California’s Zero-Emission Vehicle (ZEV) program provides rebates for FCV purchases and mandates the construction of hydrogen refueling stations. Such financial support lowers upfront costs, making fuel cell technology more accessible to businesses and consumers. However, the success of these programs often hinges on clear eligibility criteria and streamlined application processes to avoid administrative bottlenecks.

Regulatory frameworks also play a pivotal role in shaping the fuel cell ecosystem. Governments are increasingly mandating the integration of hydrogen infrastructure into existing energy systems. Germany’s National Hydrogen Strategy, for example, outlines plans to build 1,000 hydrogen refueling stations by 2030, supported by legislative measures that streamline permitting processes. In contrast, South Korea has adopted a quota system requiring a percentage of new vehicles sold to be zero-emission, including fuel cell vehicles. These policies create market demand and incentivize private sector participation, though they must be carefully designed to avoid placing undue burdens on industries still in the early stages of development.

Public-private partnerships (PPPs) are another cornerstone of government efforts to support fuel cell infrastructure. The H2USA initiative in the U.S., a collaboration between the Department of Energy and industry leaders, focuses on reducing costs and improving the performance of hydrogen infrastructure. Similarly, the UK’s Hydrogen Taskforce brings together government agencies and private companies to address challenges such as supply chain bottlenecks and public awareness. These partnerships leverage combined resources and expertise, accelerating innovation and deployment. However, ensuring equitable participation and transparent governance is essential to avoid favoring established players over smaller innovators.

Finally, governments are investing in education and workforce development to address the skills gap in the fuel cell sector. Canada’s Hydrogen Strategy includes funding for training programs in hydrogen technologies, targeting engineers, technicians, and policymakers. Such initiatives not only support the growth of a skilled workforce but also foster public acceptance by demystifying fuel cell technology. By integrating these efforts into broader energy and education policies, governments can create a sustainable foundation for the fuel cell industry, ensuring its long-term viability and accessibility.

Does RWI Stock Jetboil Fuel? A Comprehensive Guide for Campers

You may want to see also

Frequently asked questions

Yes, fuel cell vehicles (FCVs) are available in select markets, primarily in regions with established hydrogen refueling infrastructure, such as California, Japan, and parts of Europe.

Yes, fuel cell systems for residential and commercial applications, such as combined heat and power (CHP) units, are available from manufacturers like Bloom Energy and Toshiba, though adoption depends on local incentives and infrastructure.

Hydrogen refueling stations are still limited in availability, primarily concentrated in specific regions like California, Japan, and Germany, which can restrict the widespread adoption of fuel cell vehicles.

Yes, fuel cell components, such as membranes, catalysts, and stack assemblies, are readily available from suppliers and manufacturers for research, prototyping, and educational purposes.

!["QFS Fuel Cell Electrical Bulkhead Fitting 10GA Wire Fuel Pump Assembly Replacement for Universal Fit, oem allows [2] 10 gauge wires to pass through the top as well as a 3rd smaller gauge wire"](https://m.media-amazon.com/images/I/415iq52eIvL._AC_UL320_.jpg)